What the April CPI Tells Us

Six Weeks After the Petroleum Price Shock Forecast

By Jeffery W. Potter, MRED | H&M Investment Advisors, Inc. | May 12, 2026

Six weeks ago, I wrote on this site that the petroleum price shock from the war with Iran would hit American consumers in two waves. The first wave was the gasoline spike everyone saw at the pump in March. The second wave, I said, would come later. Diesel costs would work through the freight system, the food system, and the construction business over the next few months. It would show up in the data slowly, then all at once.

The April CPI came out this morning. The second wave is here.

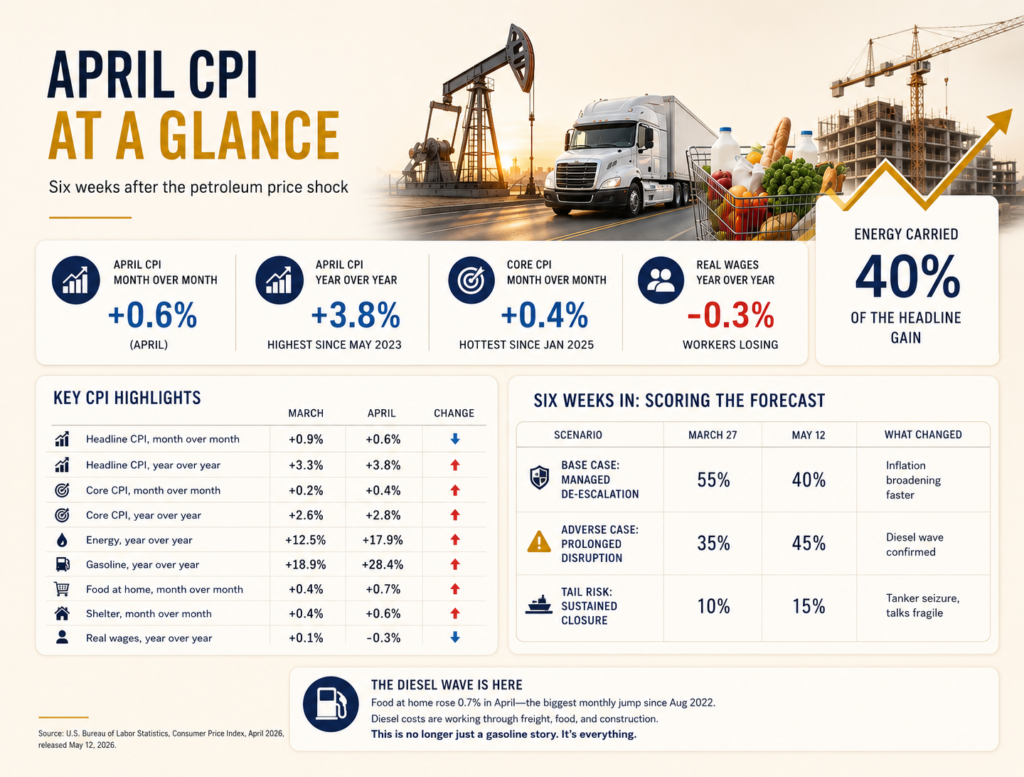

The numbers from this morning

The Bureau of Labor Statistics reported that consumer prices rose 0.6 percent in April. The annual inflation rate is now 3.8 percent. That is the highest reading since May 2023 and a half-point jump from March. Core inflation, which strips out food and energy, ran hotter than expected at 0.4 percent for the month, the biggest monthly gain since January 2025.

Source: U.S. Bureau of Labor Statistics, Consumer Price Index, April 2026, released May 12, 2026.

The diesel wave I warned about is here

On March 27, I wrote that the diesel cost shock would work through food, freight, and construction on a 60 to 120 day lag. The April numbers show exactly that. Food at home rose 0.7 percent in a single month. That is the biggest monthly jump in food at home prices since August 2022. Grocery stores are passing through their costs. Restaurants will follow.

Energy carried 40 percent of the headline gain. But the more important story is underneath. Core inflation broadened. Shelter heated up. Workers lost ground in real wages. This is what a supply shock looks like when it stops being a gasoline story and becomes everything else.

The Fed is stuck

Earlier this year, futures traders expected at least one quarter point rate cut in 2026. After this morning’s report, those same traders see zero cuts for the rest of the year. The Federal Reserve cannot cut rates with core inflation moving the wrong direction. It cannot raise rates without breaking a labor market that is already showing cracks.

Chairman Powell told the markets in March that this energy shock was, in his words, of some size and duration. He was right. He also told the markets he did not see stagflation. That call is harder to defend today than it was eight weeks ago.

Six weeks in: scoring the forecast

On March 27, I gave three scenarios with probabilities. Here is where I stand today, with the April data on the table.

I am moving the adverse case from 35 to 45 percent. The base case drops from 55 to 40. The reason is simple. The diesel wave I forecast in March arrived in the April data, and the breadth of the inflation is wider than I expected six weeks ago.

What this means on the ground

Spirit Airlines stopped flying on May 2. The company said the fuel costs killed it. That is the first big company failure I would tie directly to this energy shock, but it will not be the last. Trucking companies on spot rates without fuel hedges are the next group to watch. Restaurants with thin margins are after that. Builders dealing with diesel-heavy materials, asphalt, concrete, and steel, are working with input cost numbers nobody bid into their contracts.

In my world, real estate, this matters because operating expenses run through energy. Buildings that bought their power and gas on the spot market are getting squeezed. Buildings with fixed rate utility contracts are sitting better. The same is true for tenants. The next round of lease negotiations is going to look different from the last round.

What I am watching next

The May CPI comes out on June 11. The June CPI comes out on July 15. The May data will catch a full month of post-ceasefire freight rates and the second quarter contract resets in trucking. The June data will catch the consumer reaction. Lower income households are absorbing the gasoline and grocery shock without much cushion. We will see that in retail sales and credit card delinquencies before we see it in CPI.

Second quarter earnings calls start in mid-July. That is the first place we will hear, in plain English, which companies got squeezed and by how much. Read the trucking guidance, the retail guidance, and the airline guidance carefully.

Conclusion

In my view, the data this morning moved the picture closer to the adverse case I described in March. Inflation is broader than the gasoline story. Workers are losing ground in real wages. The Fed has no good options. The recession indicators outside CPI, the yield curve, the Sahm rule, the prediction markets, have not caught up to what the supply side is showing. They will.

I do not think we are in a recession today. I do think the second half of 2026 looks worse than the first half. Position accordingly. The May and June CPI reports will tell us whether this morning was an outlier or the start of the wave.

Jeffery W. Potter, MRED

President, H&M Investment Advisors, Inc.

California Real Estate Broker License No. 00964173

California General Contractor License No. 408893

949-891-2797 | jeffery@hminvestco.com

PotterExpertWitness.com | Newport Beach, California

Disclaimer: The information provided in this article is for informational and educational purposes only and should not be construed as financial, investment, or legal advice. While the analysis is based on publicly available data and current economic trends, future outcomes are uncertain and subject to change due to market, geopolitical, and policy developments. The views expressed are solely those of the author. Readers should conduct their own due diligence or consult a licensed professional before making decisions.